Eurodollar futures were discontinued in June 2023, successfully transitioning into 3-month SOFR futures. Short Sterling had already migrated into SONIA futures in January 2022.

Volumes in 3-month SOFR futures are as robust as they were as Eurodollar futures, ranging between 2.5 million and 4.5 million daily with healthy open interest.

So, what are the principal differences between these new RFR futures, and the legacy LIBOR linked futures?

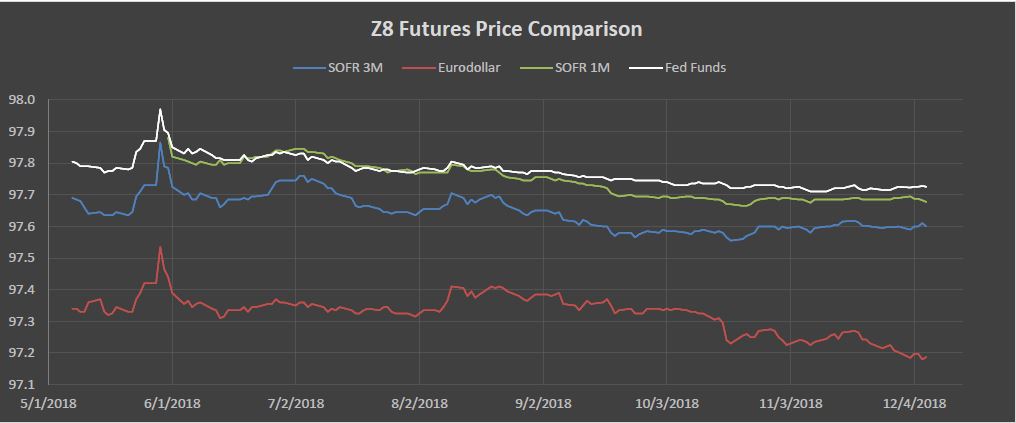

- The most obvious one is the underlying reference rate. SOFR futures reference an overnight rate derived from a broad universe of overnight Treasury repo trade activity, firmly rooted in transaction data from multiple and diverse sources. This overnight rate is essentially a risk-free rate (overnight and secured) and so contains no credit spread like (unsecured) LIBOR did. Consequently, overnight SOFR is almost perfectly correlated with the EFFR. However, 3-month SOFR futures are daily compounded market expectations of a 3-month term SOFR rate which is likely to be very different to the overnight reference rate (in fact, the correlation over a 6-week period is about 0.40 between the two)

- SOFR is an in-arrears rate whereas LIBOR was an in-advance rate. For a term 3-month borrowing or lending, the exact interest amount would be known in advance on a LIBOR transaction, but this amount would only be known in 3 months’ time for a SOFR transaction, since the interest amount would be the daily compounded rate over that 3-month period and so will not be known for sure until all daily SOFR rates in the borrowing period have been published.

- This means the quoting convention for SOFR futures will differ from those of LIBOR futures. Whereas a September Eurodollar future would confer a notional 3-month borrowing or lending from September to December but would expire and settle in September, a September SOFR future will reference a similar period but not settle until December. A September SOFR future will therefore still be live in October and November.

For example:

- The serial May 2023 SOFR future (K3) comes to final settlement on the third Wednesday of August 2023

- The interval of interest rate exposure that informs the contract final settlement price – the contract Reference Quarter – starts on the third Wednesday of May 2023 and ends on the third Wednesday of August 2023.

- The contract reference quarter for the May 2023 future spans 91 days

- From and including Wednesday, 17 May (the third Wednesday of May), until (and not including) Wednesday, 16 August (the third Wednesday of August).

- Referenced as May contract even though it settles in August.

- As a contract approaches maturity, it’s volatility should decline since most of the fixings in the compounded averaging process will already be known (SOFR will accrue as simple interest over weekends and US government securities market holidays and as compound interest otherwise)

What else is different? Well not much…

- Still quoted as 1- futures implied rate

- A basis point is still worth $25 (e.g., the difference between 95.00 and 95.01 in price terms)

- Quarterly contracts more popular than serial contracts

- Convexity bias still applies when trading SOFR futures against Swaps and Treasuries

- All the spreading opportunities that were available using Eurodollar futures still remain, they are just likely to be less volatile, particularly for inter-contract spreads due to the lack of a credit element.