Are changes in Euribor fixings correlated with movements in the Euribor implied forward rates?

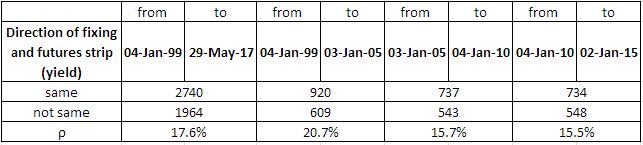

Intuitively, we might think so but empirical evidence suggests otherwise. Given a data set from January 1999 to May 2017, there were 2740 days when a change in the Euribor fixing was replicated with a similar movement in the implied forward rates of the white pack and 1964 days when they were not. This results in a low correlation of just 17.6%. Breaking the data into smaller 5-6 year buckets does not demonstrate causality between the direction of Euribor fixings and movements in the Euribor futures implied forward curve.