Welcome to STIR futures

This is a supporting website for those who want to go beyond the book. Enjoy…

Menu

Skip to content

Home

Stephen Aikin

Forum posts

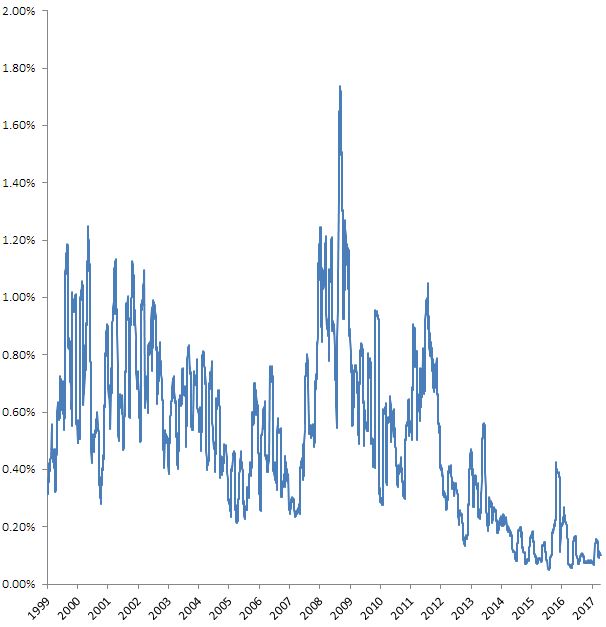

Declining Euribor volatility

June 3, 2017

by

Stephen

Post navigation

←

Policy rate tightening

Causation between 3M Euribor fixings and Euribor futures rates

→

Click the book for more info