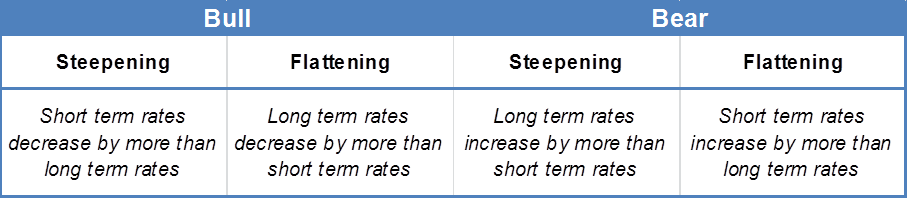

Many short term rate traders trade the ever changing term structure of rates, called the (yield) curve. Generally, most curve movements can be classified as steepeners (where the differential between long term rates minus short term rates widens) or flatteners (the opposite). They can be further differentiated by bull/ bear steepening/flattening:

One big question remains though – will the curve steepen or flatten? There are many curve drivers but an interesting one is the relationship between short rates like 3-month LIBOR or EURIBOR and steepening or flattening phases.

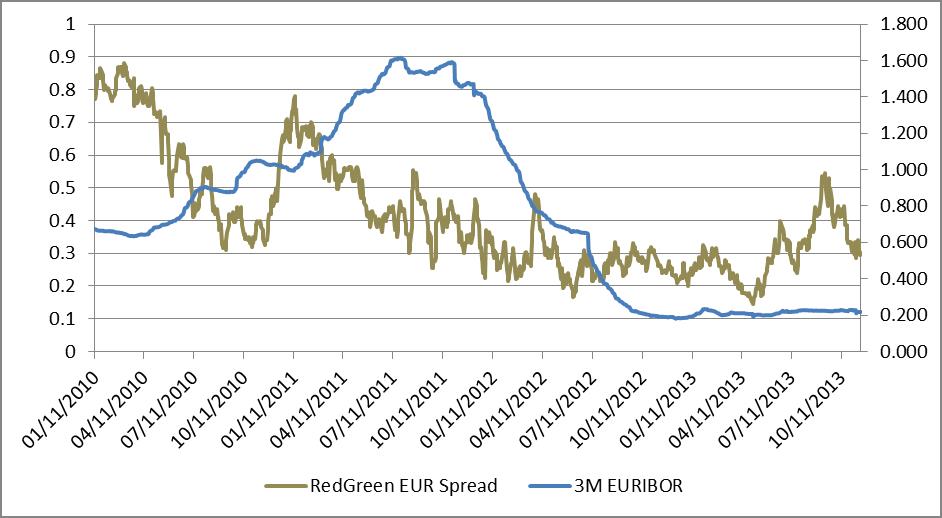

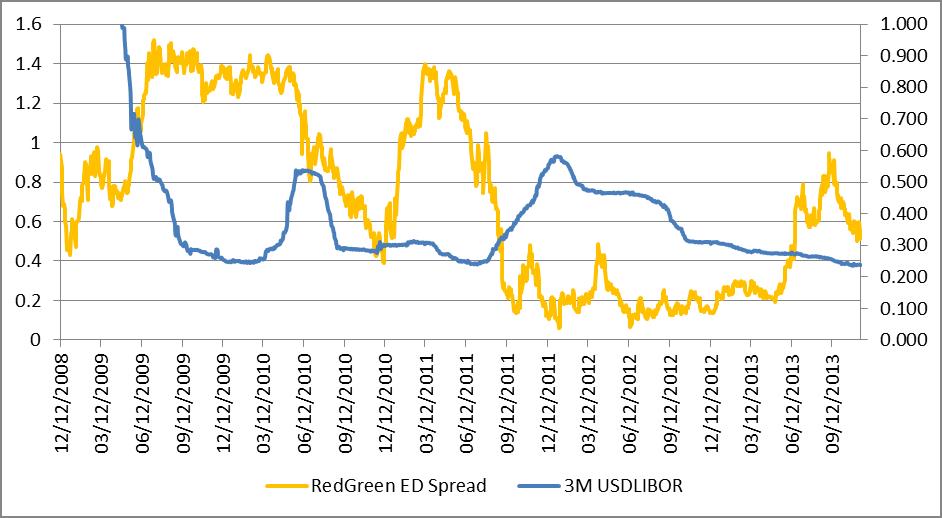

The chart below shows this relationship for 3-month USD LIBOR (RH scale) and the RedGreen one year Eurodollar calendar spread (LH scale)

The RedGreen one year Eurodollar calendar spread is the spread between the first red Eurodollar futures and the first green Eurodollar future, rolled every quarterly expiry, expressed in rate terms

(100-Green)-(100-red)

An increase in this spread means the curve is steepening and a decrease means it is flattening.

There is a causal link relationship between the short rate and the state of the curve.

Generally,

- when short rates rise, the curve flattens

- As policy rates increase, pushing money market rates higher, the short end of the curve increases more quickly than the longer end, hence flattening. This is technically a bear flattening.

- And when short rates fall, the curve steepens for the opposite reasons. This is a bull steepening.

Here’s the same for the Euribor.