Risk free interest rates (RFR) like SOFR for USD are replacement rates for Libor. Unlike Libor, RFR do not include a credit spread component and so a spread adjustment is added to the RFR to account for the difference. This spread adjustment is the fallback spread to be used for legacy LIBOR linked contracts when LIBOR publication has been discontinued. There is likely to be different fallback spreads used for cash products and derivatives and ISDA has published their fallback adjustment for derivative markets as follows:

Compounded setting in arrears RFR rate + spread adjustment based on the median spot spread between the IBOR and the term-adjusted RFR calculated over a static lookback period of five years prior to the Index Cessation Event

The index cessation event is a public statement by the LIBOR regulator or administrator that publication has ceased or will cease and result in fallback spreads being fixed and applied as a spread adjustment to the RFR to create an “all-in” fallback rate.

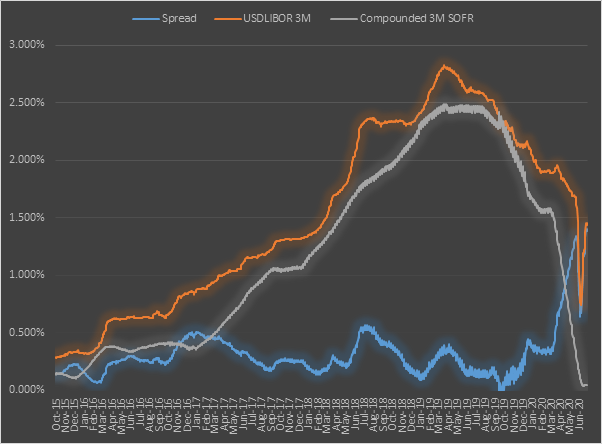

If index cessation event happened today fixing the fallback spread for 3m USD, it would cover a period from December 2015- December 2020 and would be about 26bps (see chart). In contrast, if a cessation were announced in June 2023 then the spread would cover a period from June 2018 to June 2023 and is likely to be lower than 26bps because higher levels of the fallback spread in 2016 drop out of the dataset that the 5Y median references.

ISDA 3m USD Fallback spread Jun 2015-June 2020. 5Y median = 26bps

During November 2020, the market was expecting a cessation announcement sometime during 2021 and was pricing fallback spread expectations c. 26bps, to be applied as part of an all-in rate shortly after December 2021. On 30th November, IBA effectively announced an extension of the discontinuation timeline for US Libor to mid-2023. This caused the market to price expectations that fallback spreads would apply to Eurodollar futures settling post June 2023 based on a spread calculated from a 2021 cessation event. This caused pre-June 2023 contracts to rally relative to contracts settling post-June 2023 since they would now settle to actual Libor perceived to be lower than the “all-in” rate to be applied post-June 2023. The 4th December ISDA announcement effectively ratified this pricing adjustment.