Stir futures are, of course, futures on short term interest rates, primarily IBORs (interbank offered rates). The Eurodollar and Short Sterling are based on LIBOR (London Interbank Offered Rate) and the Euribor is named after its underlying reference rate – EURIBOR (Euro Interbank Offered Rate).

Because of the LIBOR/EUROBOR fixing scandals, plus operational aspects like the lack of volume and submission and fixing methodology, the FSB (Financial Stability Board) published a report in 2014 on “Reforming Major Interest Rate Benchmarks” which provided the basis for the FCA’s (Financial Conduct Authority) decision to sustain LIBOR until the end of 2021. After that, panel banks will no longer be required to submit LIBOR rates, which likely lead to the demise of LIBOR as a reference rate and remove the demand for derivatives based upon it.

As an alternative, the following have been adopted as reference rates

USD: Secured Overnight Financing Rate (SOFR)

EUR: Euro Short-term Rate (ESTER)

JPY: Tokyo Overnight Average Rate (TONAR)

GBP: Sterling Overnight Index Average (SONIA)

CHF: Swiss Average Rate Overnight (SARON)

SOFR is a fully transaction-based reference rate, derived from a composition of repo rates – General Tri-Party (Bank of New York Mellon), DTCC cleared General Collateral and Bilateral FICC cleared. SOFR daily trading volume is around $800 B which is about 1500 times the daily LIBOR transaction volume.

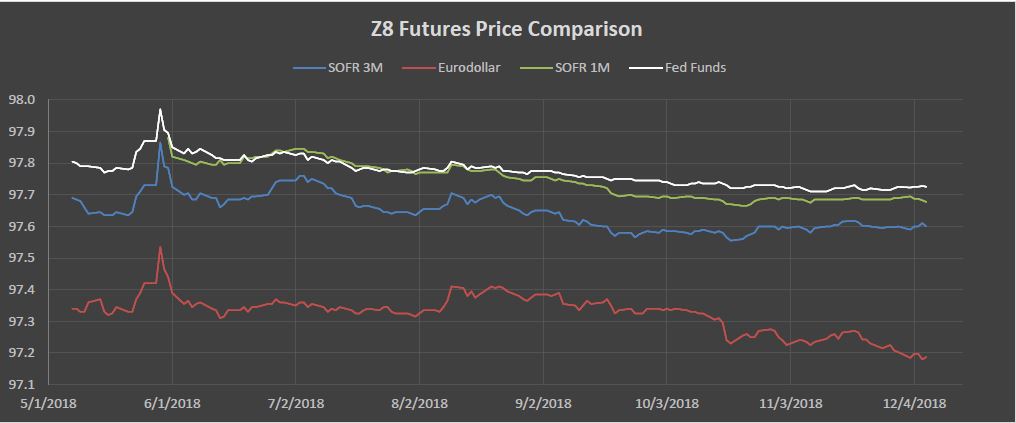

In the US, SOFR futures were introduced by CME in May 2018 and because they are based on a secured financing rate (in contrast to LIBOR being based on unsecured financing), the SOFR futures trade at a higher price (lower rate) that Eurodollar futures.

Source: Bloomberg

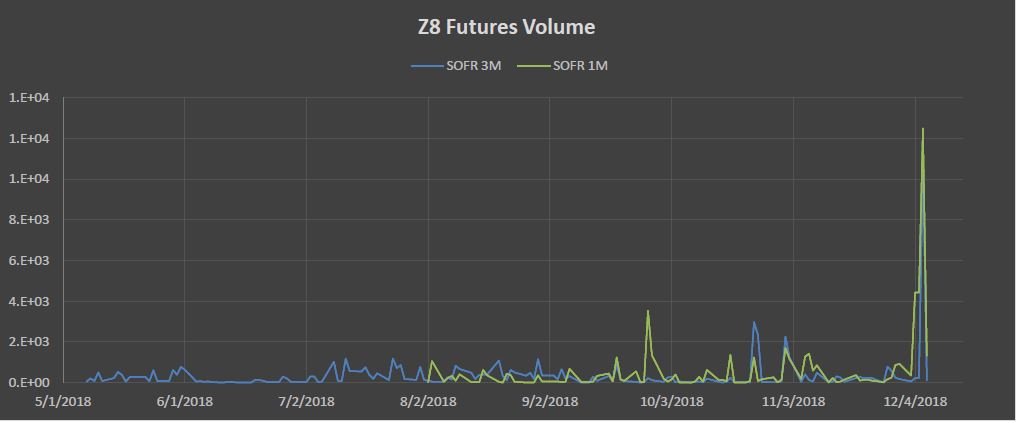

Volumes are increasing

Source: Bloomberg

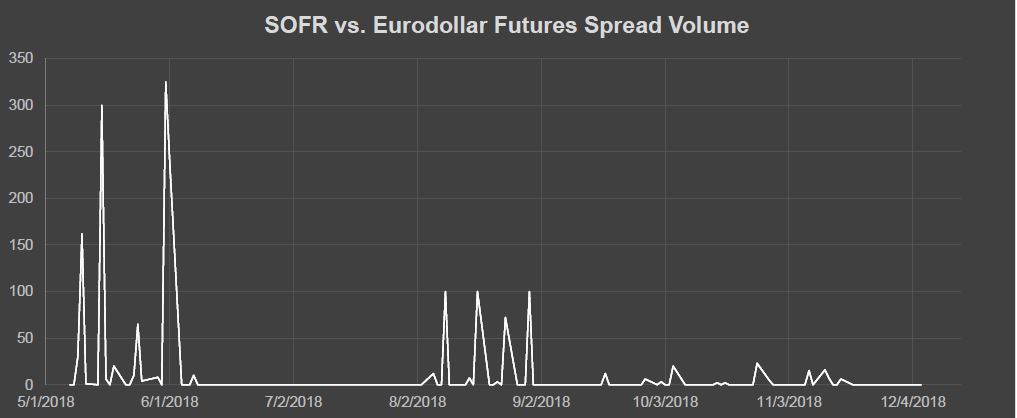

And a developing market in inter contract spreads

Source: Bloomberg

Based on a presentation by Numerix